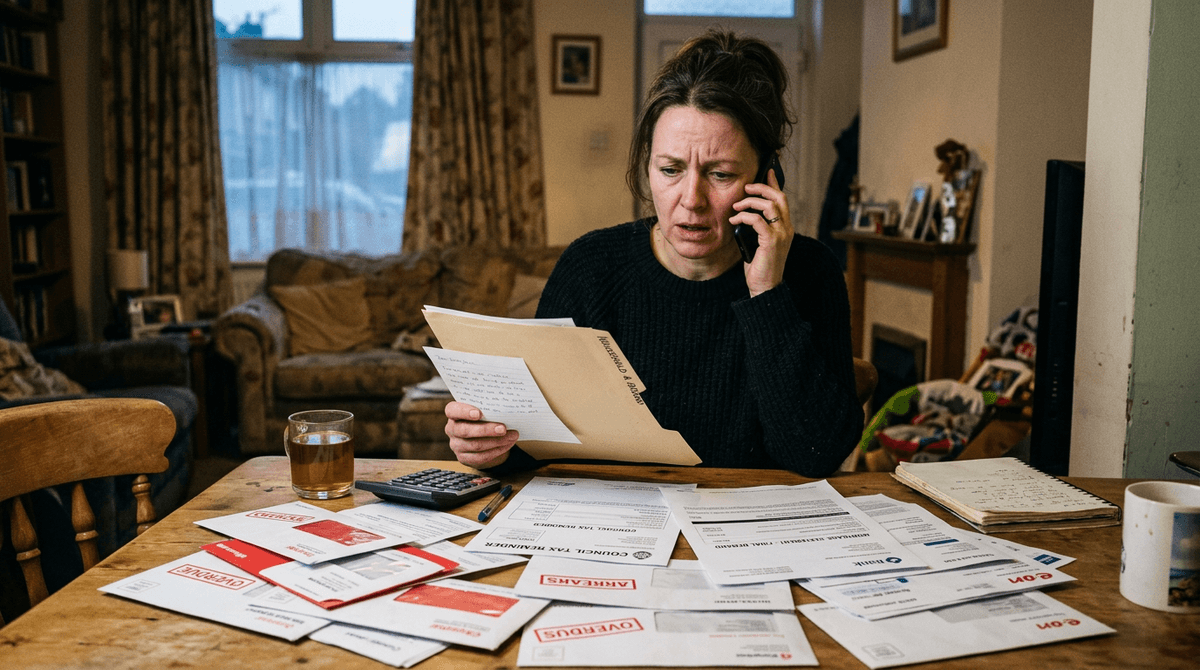

The gap before the DMP begins feels risky

Between deciding on a Debt Management Plan and the day it actually starts, there’s often a stretch where nothing feels “in place” yet. You’re still due to pay everyone, but you’re also trying to ringfence money for rent, council tax, food, travel, and the first DMP payment. If you keep paying minimums across the board, it can look tidier on paper, but it’s common to arrive at the start date short of cash and end up missing essentials or the first DMP contribution.

If you pause payments, the budget usually breathes straight away, which is often the point. The trade-off is that the account status changes quickly: missed-payment markers, extra interest, and letters landing closer together. It can feel like you’ve “made it worse” in a fortnight, even though what you’re really doing is accepting short-term mess to stop the longer-term drift.

The risk isn’t just credit-file damage; it’s timing. A DMP works when the income-and-expenditure is realistic and repeatable. A few weeks of trying to keep everyone happy can quietly undermine that before it’s even begun.

What creditors typically do when payments pause

The first thing that usually happens is boring but relentless: a missed payment triggers an automated cycle. A text or email, then a letter, then the “please call us” messages. If the account has late fees or daily interest, the balance can tick up while you’re sitting there trying to get the DMP start date confirmed.

After that, the tone changes. Some lenders restrict the card, reduce the limit, or move the account to their collections team. Calls can start coming at awkward times, and the paperwork gets thicker, even if you’ve already told them you’re setting up a plan.

If the pause runs on, you may see formal arrears notices and, later, a default notice. That isn’t rare; it’s often just the creditor’s process catching up with your timing.

When continuing minimums quietly helps later negotiations

There are cases where keeping a minimum going, quietly, buys you breathing space with that creditor later. If an account stays “up to date” for another month, it often avoids an immediate hand-off to collections, which means fewer calls, fewer late fees, and less chance of a default notice landing before the DMP paperwork is even finished.

It can also help when you ask for interest to be stopped. A lender who’s seen you keep paying something right up to the point the DMP starts may be less defensive than one who’s had two missed payments and a complaint file opened at the same time.

The catch is cash. Minimums across the board can drain the money you actually need for rent, council tax, travel, and the first DMP contribution. So this only works when it’s targeted, affordable, and time-limited.

The common workaround: token payments and scripts

When the money’s tight but you can’t face going completely silent, people often do a “token” payment for a few weeks — £1 or £5 — to show willing while keeping enough back for essentials and the first DMP payment. It doesn’t stop late markers, and it won’t prevent interest on most accounts, but it can soften the tone of the contact and buy a bit of calm while the plan date is confirmed.

The friction is practical: if you pay by direct debit, you may need to cancel it and make the token by bank transfer so you stay in control. Some lenders will still chase; the point is avoiding an accidental minimum leaving you short on rent or council tax that same week.

What you say matters less than keeping it consistent: “I’m setting up a Debt Management Plan. I can pay £5 today as a holding payment. Please note financial difficulty and pause interest and charges. I’ll send my DMP provider details as soon as I have the start date.”

A reasonable choice that can backfire fast

It’s very common to pick one “scary” creditor and keep them sweet for a few weeks. Maybe it’s the card with the highest limit, or the lender that rings most. On paper it feels sensible: one less fire to put out while the DMP date is being lined up. In practice, it can tip the whole month. A £120 minimum to one card can be the petrol money and groceries that were meant to get you through to payday, and then the council tax bounces and the stress just moves sideways.

The fastest way this backfires is when those payments are coming out by direct debit. You think you’ve budgeted, then two lenders lift full minimums on different days, the overdraft is swallowed, and suddenly you’re paying charges on your bank account as well as the debts.

Worse, you can arrive at the DMP start date short, miss the first contribution, and lose momentum right when you needed stability most.

Priority debts that change the whole answer

If there’s any “priority” debt in the mix, the question stops being “should I keep creditors happy?” and becomes “what must not be allowed to slip?” Rent or mortgage, council tax, gas/electric, TV Licence, child maintenance, and anything with court enforcement sitting behind it can move faster than a credit card ever will. Miss the wrong thing for two weeks and you can be dealing with arrears letters, enforcement agents, or a prepayment meter, right when you’re trying to stabilise.

That’s why some people pause all unsecured payments before a DMP, even if it feels messy, and push every spare pound into keeping the roof, council tax, and essentials straight. The credit cards can shout; the landlord and the council can act.

It’s also where a “holding payment” to a lender is the first thing to drop. If paying £5 means the council tax instalment fails, it wasn’t a goodwill payment — it was a mistake.

A practical checklist for deciding this week

Start with the dates, not the feelings. List what must be paid before your DMP goes live: rent or mortgage, council tax, gas/electric, water if you pay it directly, travel to work, food, prescriptions, childcare. Put the due dates next to your payday, and leave a buffer for one mistake (a direct debit you forgot, a bill that comes early). If you can’t cover that list and the first DMP payment, you already have your answer: unsecured creditors get paused or token payments only.

Next, check the mechanics. Cancel direct debits to credit cards/loans if there’s any chance they’ll take full minimums and knock you off balance; keep control with manual payments. Tell your DMP provider exactly what you’re doing so the first contribution doesn’t get built on money you’ve already sent out. If you do pay anything, make it targeted and time-limited: one or two accounts, small amounts, until a clear start date is confirmed.

Finally, decide what you can live with for a month: more calls and letters, or a tighter budget that risks rent/council tax slipping. Either way, write a simple note to each creditor: DMP being set up, what you can pay this week (or that you can’t), and when you’ll send the provider details.